What Changes at 71 – and Why It Matters

For most of your financial life, retirement planning has a single objective: accumulate: contribute to your RRSP, reduce your taxable income, and let the investments grow tax-deferred for as long as possible. The government effectively lends you the tax money on every contribution, interest-free, for decades. It is one of the most powerful wealth-building tools available to Canadians.

But the RRSP has a deadline. By December 31 of the year you turn 71, it must be converted into a Registered Retirement Income Fund (RRIF). The conversion itself isn’t a taxable event. Your investments aren’t sold. The money stays exactly where it is. Only the ‘container’ changes.

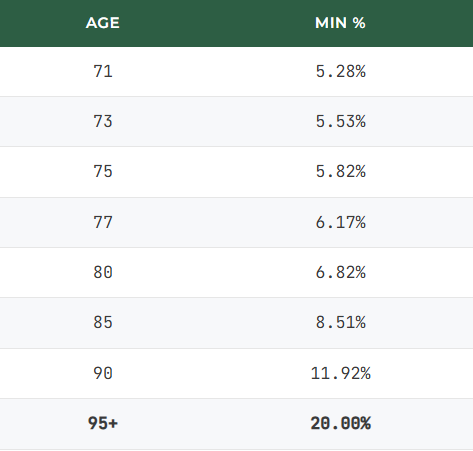

The new container changes the direction of money flow. Your RRSP was designed to take money in. Your RRIF is designed to push money out in accordance with a schedule set by the CRA. Every year, the government requires you to withdraw a minimum percentage of your account’s value. That percentage starts at 5.28% at age 71 and rises every year for the rest of your life.

There is no maximum to how much you can draw from your RRIF; however, every dollar that leaves the account is taxed as ordinary income. The bank withholds tax only on amounts above the minimum; the tax owing on the minimum itself is then settled when you file your annual return.

How RRIF Withdrawals Are Taxed

Suppose you hold a $500,000 RRIF at age 72. Your CRA minimum withdrawal for the year is 5.40%, which works out to $27,000.

Your financial institution deposits the full $27,000 into your bank account. No tax is withheld at source as that is the rule for minimum withdrawals. However, that $27,000 is added to your taxable income for the year. If your combined marginal tax rate is 33%, you will owe approximately $8,910 when you file your annual return. This is worth planning for, because the tax bill arrives months after the money was deposited.

You decide you need to withdraw $50,000 this year. The first $27,000 (the minimum) is deposited without withholding, exactly as in Scenario A. The remaining $23,000 is subject to mandatory withholding at graduated rates:

On the first $5,000 of the excess: 10% withheld = $500. On the next $10,000: 20% withheld = $2,000. On the remaining $8,000: 30% withheld = $2,400. Total withheld at source: $4,900.

You receive $45,100 in your bank account ($50,000 minus $4,900). But at filing, the full $50,000 is taxable income. At a 33% marginal rate, the total tax owing is approximately $16,500. You’ve already paid $4,900 through withholding, so you’ll owe an additional $11,600 at tax time.

The key point: withholding is not the same as taxation. The graduated rates withheld at source (10/20/30%) are often less than your actual marginal rate. Many retirees are surprised by a balance owing at tax time because they assumed the withholding covered the full tax. It often doesn’t, particularly for those with other sources of retirement income. Tax amounts shown are illustrative; individual results will vary based on province of residence, total income, and applicable credits. Consult a tax professional for your specific situation.

This creates a new job for your investments. During accumulation, the only thing that mattered was growth. Inside a RRIF, your portfolio has to do two things at once: generate enough income to cover mandatory withdrawals, and preserve enough capital to sustain the account across a retirement that could last two or more decades. That’s a fundamentally different assignment and the investment that was best suited to the first job isn’t necessarily the right one for the second.

How Tax Sheltering Works Inside a RRIF

Before we get to the risk side, there’s a foundational concept worth understanding because it reshapes how you should think about what belongs inside a RRIF.

In a non-registered (taxable) account, the type of income your investment generates determines how much of it you keep. Interest income from bonds, GICs, mortgage funds is taxed at your full marginal rate. For a high-income retiree in Ontario, that can exceed 53%. Eligible dividends are taxed more favourably, thanks to the dividend tax credit. Capital gains receive preferential treatment through a lower inclusion rate, though that rate has changed in recent years and varies by the amount of gain realized. This is why many financial advisors steer clients away from interest-generating products in taxable accounts. The tax drag is real. For example, on a 9% yield taxed entirely as interest at a 53% marginal rate, a retiree might keep less than 4.5% after tax. The same 9% realized as a capital gain would, depending on the inclusion rate and amount, leave closer to 6.5%. Individual results vary by province, income level, and the nature of the gain.

Inside a RRIF, that entire framework disappears.

All income types, interest, dividends, capital gains, are sheltered equally while they remain in the account. Tax only applies when you withdraw, and at that point the CRA does not distinguish what generated the income. Interest is treated the same as capital gains. The preferential treatment that dividends and capital gains receive in a taxable account simply doesn’t exist in a registered account like RRSP and RRIF. All three income types are treated identically.

In practice, this has a direct implication. An investment that would be heavily penalized by the tax code in a non-registered account, say a high-yield mortgage fund generating 100% interest income, becomes just as tax-efficient as a growth stock the moment it sits inside a RRIF. The structural disadvantage that kept it out of your taxable portfolio doesn’t apply here.

Same Fund, Different Account

Suppose you invest $500,000 in a mortgage fund yielding 9% annually producing $45,000 in income. Here’s what happens in two different accounts, assuming an Ontario retiree with a combined marginal rate of approximately 43%.

The $45,000 is classified as interest income and taxed at your full marginal rate. Tax owing is approximately $19,350. After tax, you keep $25,650, which is an effective yield of about 5.1% on your capital.

The same $45,000 compounds within the account with no tax applied at all. If your CRA withdrawal minimum is $27,000, that amount is withdrawn and taxed at your marginal rate but the remaining $18,000 stays inside the RRIF and continues to compound, fully sheltered. No portion of the income is taxed at source, and the surplus grows as though no tax existed.

Over a single year, the illustrative difference is roughly $18,000 in additional sheltered capital. Over ten years of compounding, the gap between these two scenarios grows considerably, not because the investment changed, but because the account it sits in determines how much of the return you get to keep and reinvest. Tax outcomes depend on individual circumstances including province of residence and total income.

Once you understand this, the question shifts. It’s no longer “what type of income does this investment generate?” It’s something simpler: how much does it yield and how reliably does it do so?

This inverts the logic many investors carry into retirement. The products you avoided for years because of their tax profile may actually be the ones best suited to the account you’re now managing.

Sequence-of-Returns Risk: What is it and Why is it important

This is the most important concept in this article and the one least understood by most Canadians entering retirement.

During the accumulation phase, a market downturn is painful but manageable. If your portfolio drops 12% in a given year, you can stop contributing, hold steady, or even buy at lower prices. When the market recovers, your portfolio recovers with it. Time is on your side. The loss is temporary.

In a RRIF, that logic does not apply and the reason is mathematical, not emotional.

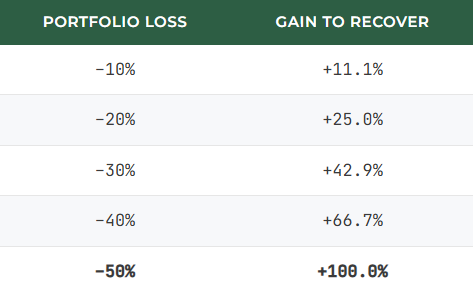

There is an asymmetry of losses. Percentage losses and percentage gains aren’t symmetrical. This is a basic mathematical property, but it surprises many investors when they see it laid out clearly. A 10% loss doesn’t require a 10% gain to recover. It requires 11.1%. A 20% loss requires 25%. A 50% loss requires a 100% gain just to get back to where you started.

On its own, this asymmetry is manageable during accumulation. You have decades of contributions ahead of you, and compound growth eventually overcomes it. But inside a RRIF, it becomes more consequential.

Impact of drawdown in an account

Start with a $1,000,000 RRIF in a 60/40 portfolio. In Year 1, the equity market drops 20%.

Your portfolio falls to $800,000. To get back to $1,000,000, you need a $200,000 gain. $200,000 ÷ $800,000 = 25%. So a 20% loss requires a 25% gain just to break even. That’s the asymmetry at work.

Now add the CRA minimum withdrawal. At age 71, 5.28% of your January 1 balance (against the $1,000,000 at that date) must be withdrawn. That’s $52,800 leaving the account. Your balance at year-end: approximately $747,200.

To return to $1,000,000 from $747,200, you now need a gain of $252,800, a 33.8% return. And next year, the CRA minimum withdrawal rises again, and another withdrawal is required regardless of where markets stand.

This is how the two forces compound against each other. The market loss creates a recovery deficit. The mandatory withdrawal deepens it. And each subsequent year of withdrawals makes the hole slightly harder to climb out of even if markets are recovering.

The compounding effect of forced withdrawals. In a RRIF, the CRA requires you to withdraw a minimum every year regardless of what the market has done. When your portfolio drops and you’re simultaneously forced to sell units to fund a withdrawal, you’re locking in losses. That capital leaves the account permanently. It doesn’t participate in the recovery and the base from which your portfolio needs to recover has now shrunk by both the market loss and the withdrawal.

This is what’s meant by sequence-of-returns risk: the danger that poor returns arrive early in the decumulation phase, at the exact moment when your account is at its largest and mandatory withdrawals are pulling capital out.

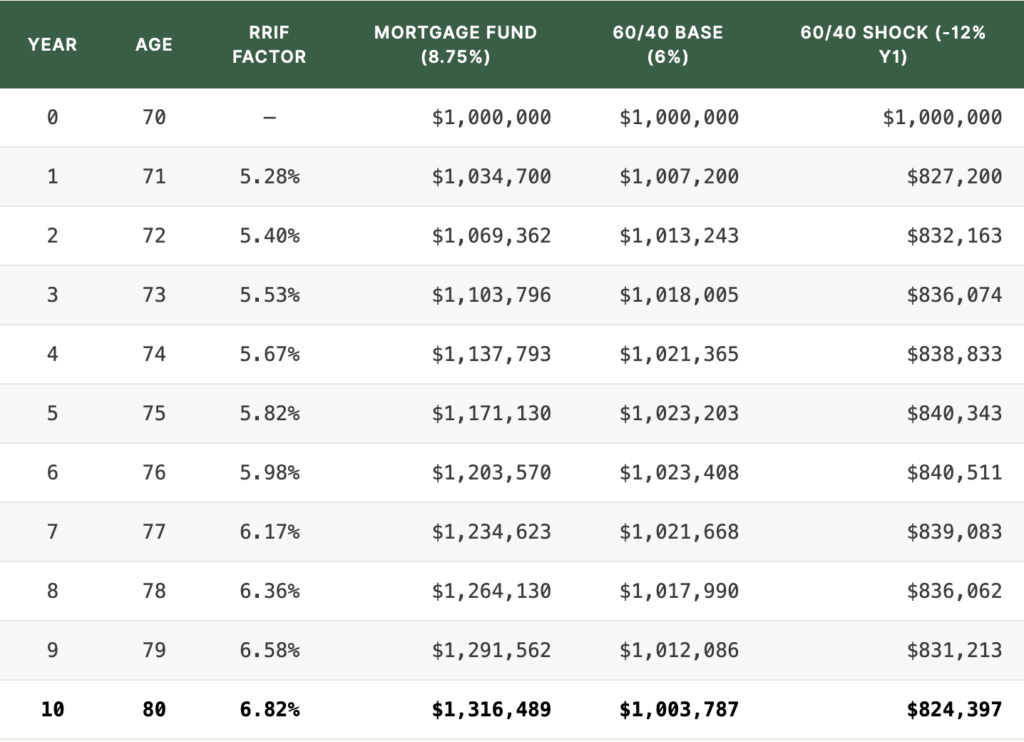

Let’s walk through it with real numbers. Imagine a $1,000,000 portfolio in a standard 60/40 equity-bond allocation. In Year 1 of your RRIF, the equity market drops 12%. That’s not a crisis, it’s a routine bear market correction, roughly in line with the average intra-year drawdown of the S&P 500.

Your $1,000,000 becomes $880,000 on paper. Then the CRA requires your 5.28% minimum withdrawal. That’s calculated on the January 1 balance, $1,000,000, so $52,800 leaves the account. Your balance at the end of Year 1: approximately $827,200. You’ve lost 17.3% of your RRIF portfolio in a single year, and you needed to withdraw $52,800 of it at the worst possible time.

Now assume the market recovers and averages a steady 6% for the remaining nine years:

All projections are hypothetical illustrations. For simplicity, annual return is applied before accounting for withdrawals for each particular year. The mortgage fund column assumes the target 8.75% annual distribution is achieved consistently with no capital losses or borrower defaults. The 60/40 columns assume a blended 6% annual return (base) or –12% in Year 1 followed by 6% annually (shock). CRA minimum withdrawal factors applied as legislated. Actual investor outcomes will vary. Target yields are not guaranteed.

Look at the “60/40 Shock” column. After a full decade of recovery, nine consecutive years of positive returns, the portfolio reaches $824,397. Essentially maintaining the Year 1 balance. A decade of compounding, consumed by a single bad year that happened to arrive first.

Now compare that to the “60/40 Base” column, which assumes a calm, steady 6% every year with no shock. Even in that scenario, the portfolio barely grows. After ten years of mandatory withdrawals, it sits at $1,003,787. The withdrawals eat nearly all of the growth.

What this means for monthly income at Age 80

At age 80, the CRA minimum withdrawal is 6.82%. Let’s translate each projected ending balance into the annual income the account would be required to distribute and what that looks like month to month. These figures assume the target yields described above are achieved consistently and no capital losses occur.

Minimum withdrawal: 6.82% × $1,316,489 = $89,785 per year, or approximately $7,482 per month. Because the fund targets 8.75%, it would continue generating income above the minimum with the surplus staying in the account to compound further, assuming the target distribution is maintained.

Minimum withdrawal: 6.82% × $1,003,787 = $68,458 per year, or approximately $5,705 per month.

Minimum withdrawal: 6.82% × $824,397 = $56,224 per year, or approximately $4,685 per month. The impact of the initial shock in Year 1 is clear.

The projected difference between the mortgage fund and the balanced portfolio at age 80 is approximately $1,777 per month in retirement income from the same $1,000,000 starting point, under the same CRA rules. These projections are hypothetical illustrations based on the stated assumptions; actual outcomes will vary.

Here is the point worth understanding clearly: in a RRIF, a balanced portfolio needs to earn its return and fund the CRA’s withdrawals and overcome the asymmetry of any losses. When all three forces act together, the margin for error is extremely thin.

*Projections assume target yields are achieved consistently with no capital losses or borrower defaults. Target yields are not guaranteed. See offering memorandum for complete details and risk factors.

The mortgage fund column tells a different story. Because the return is generated from contractual borrower interest payments rather than market appreciation, it is not directly correlated to equity market movements. The Net Asset Value is designed to remain stable, though it is not guaranteed and can be affected by borrower defaults or impairments in the underlying mortgage portfolio. Assuming the fund achieves its target yield with no capital losses, withdrawals come from income, not from selling assets at depressed prices. The projected result after ten years: $1,316,489, more than $312,000 ahead of the balanced portfolio, even in calm conditions.

What You Give Up and What You Should Know

Any honest discussion of an investment strategy has to include what you’re giving up. Moving away from a public market portfolio and into a private mortgage fund involves real trade-offs, and they’re worth understanding clearly.

Liquidity. In a public equity portfolio, you can sell your holdings on any business day. In a private mortgage fund, you can’t. Redemptions are typically subject to notice periods and may be limited by the fund’s available cash. If you need to access a significant amount of capital quickly, a private fund is not designed for that. This is the fundamental exchange: you’re trading public market liquidity for private market income stability.

In-kind deregistration risk. This is a scenario worth understanding even if it’s unlikely. If a private fund doesn’t generate enough cash to meet the CRA’s mandatory minimums in a given year due to borrower defaults, market stress, or liquidity constraints. The result can be what’s called a taxable in-kind deregistration. The custodian is forced to deregister the illiquid units to satisfy the CRA requirement, and you owe the tax on their fair market value immediately. This doesn’t mean you’ve lost the investment, but it does mean you’ve lost the tax deferral which can be a significant cost.

The cost of advice. This isn’t specific to mortgage funds, but it’s worth mentioning because it affects RRIF returns broadly. When you hold investments through an advisor-managed platform, you’ll typically pay an annual fee of 1% to 2% of your total assets. That fee is deducted whether your portfolio grew or not. On a $1,000,000 RRIF paying a 1.5% annual fee, that’s $15,000 a year leaving the account on top of your CRA minimums. Over two decades, the drag is substantial. In a self-directed RRIF, those fees don’t apply. It’s one of the most underappreciated variables in retirement income planning.

The Long-Term Cost of a 1.5% Annual Fee

Suppose two investors each hold a $1,000,000 RRIF invested in the same fund yielding 6% gross. One holds it self-directed (no advisor fee). The other pays a 1.5% annual management fee, reducing the net return to 4.5%.

The self-directed investor’s account balance: approximately $985,000. The advisor-managed investor’s account balance: approximately $790,000. The difference: roughly $195,000 entirely attributable to the fee. No change in the underlying investment, no difference in CRA rules, no difference in market returns. These figures are illustrative and assume consistent 6% gross returns throughout; actual outcomes will vary.

A 1.5% fee sounds modest in isolation. But inside a RRIF, where the account is already being drawn down by mandatory withdrawals, the fee acts as a third drain alongside the CRA minimums and any market losses. Over a long retirement, the cumulative impact can be equivalent to several years of income.

The decision isn’t whether one approach is universally “better.” It’s whether the specific trade-offs of private market investing, lower liquidity, less daily transparency, longer time horizons, are ones you can accept in exchange for the income stability that a RRIF structurally requires.

How We Approach This Problem

Everything above applies to private mortgage funds as a category. This section is about how Morrison Financial specifically operates within that category and why, in our view, the structure is well suited to the RRIF challenge described in this article.

Morrison Financial Mortgage Income Funds are not a REIT. They don’t own property. They don’t rely on occupancy rates, lease renewals, or property valuations to generate income. What it does is lend capital, secured against real property. Borrowers pay interest under the terms of a mortgage contract. That interest flows to investors as monthly distributions. The income is contractual, determined by the terms of the mortgage agreements, not by what the stock market did this morning. The borrower owes the interest under the terms of the mortgage contract, though as with any lending arrangement, borrower default remains a risk, which is why conservative underwriting and loan-to-value discipline are central to the fund’s approach.

The yield spread. Morrison Financial Mortgage Income Funds target an effective annual return of 8.75%, distributed monthly. At age 71, when the CRA requires a 5.28% withdrawal, achieving the target distribution would generate a surplus of approximately 3.47%. Assuming the fund meets its target, that surplus stays inside the RRIF and continues to compound, tax-deferred. By age 80, when the minimum reaches 6.82%, the fund’s target yield would still generate a spread of nearly 2% above the requirement. Target yields are not guaranteed, but this spread is what the fund is designed to produce.

A protected position in the capital stack. Morrison Financial’s mortgage funds occupy the senior debt position. Borrower equity absorbs the first 20–35% of any decline in property value before the fund’s capital is exposed. This structural buffer is designed to reduce the fund’s exposure to routine real estate fluctuations though it does not eliminate capital risk entirely. No investment in private lending is without risk of loss.

Self-directed structure. Morrison Financial’s funds are held through Olympia Trust in a self-directed RRIF. That means no advisor management fees layered on top of the fund’s return. The custodians (e.g. Olympia Trust, Questrade) handle all CRA reporting, T4RIF tax slips, and withdrawal processing. The conversion from RRSP to RRIF does not affect your holdings, meaning your units, your distributions, and your participation in the fund’s mortgage portfolio remain exactly the same.

Track record. Morrison Financial has been lending against Canadian real estate for nearly 40 years. It has funded over $1.6 billion in mortgage loans across more than 650 completed transactions. The fund’s income has historically exceeded mandatory CRA minimums from age 71 through 85, though past performance is not indicative of future results.

When target distributions are achieved, withdrawals come from income and not from selling down the capital you spent a lifetime building. That’s not a marginal difference. It’s a structural one. Target distributions are not guaranteed.

Disclaimer:

Morrison Financial is one of Canada’s longest-standing private real estate finance firms. During its 38 years in business, Morrison Financial has advanced over $1.6 billion in loans. Morrison Financial operates two private mortgage income funds which invest in a diversified portfolio of short-term residential development projects across Ontario, and its trust units are eligible to be held in registered accounts.

This material is not financial advice and is for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. Morrison Financial’s Mortgage Income Funds are offered exclusively through Belco Private Capital to investors under applicable securities legislation. Prospective investors must review the offering memorandum in its entirety prior to making any investment decision. Private exempt market securities are illiquid and are not suitable for all investors. Yields are targeted and not guaranteed. Past performance is not indicative of future results. All projections are hypothetical illustrations based on stated assumptions and do not represent actual investor outcomes. Tax information presented is general in nature and may not reflect your individual circumstances; consult with independent tax and legal advisors.

Contact us to schedule a time with one of the dealing representatives to determine whether this investment is suitable for you.

Article by:

Matthew Solda, MBA – Vice President