A $130,000 combined potential rebate, a twelve-month window, and a set of mechanics that change how new homes price, sell, and finance.

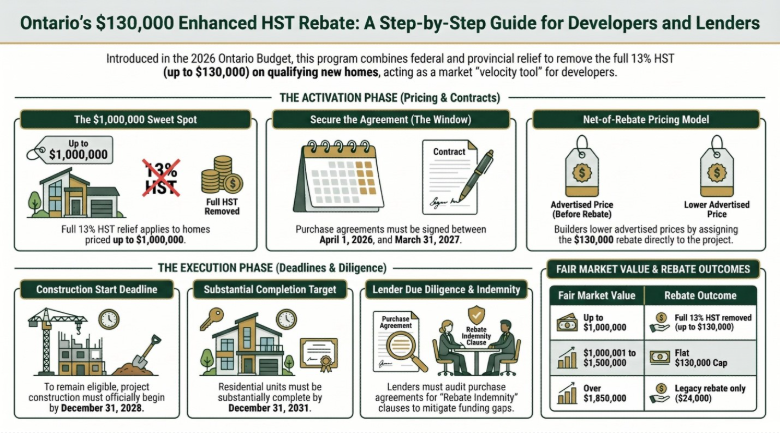

On March 26, 2026, the Ontario Budget introduced a one-year enhanced new housing rebate program that effectively removes the full 13% HST on qualifying new homes. The qualifying rebate can reach a maximum of $130,000 for first time home buyers, move-up buyers, and investors.

This enhanced program aims to spark market activity in Ontario, which has largely been stalled over the past few years. The government projects approximately $2.2 billion in total tax relief and 8,000 additional housing starts in Ontario over the life of the program. This article covers our interpretation of the program structure and eligibility, and our perspective as a commercial mortgage lender.

The Rebate Programs

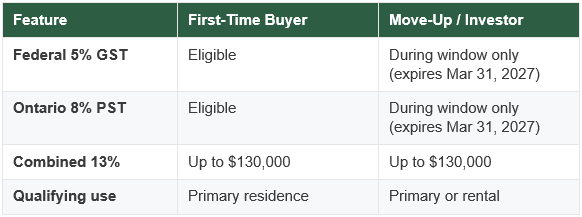

Federal level – 5% GST rebate under Bill C-4 (the Making Life More Affordable for Canadians Act): The federal program eliminates the 5% GST component of HST, to a maximum of $50,000. Full relief applies up to $1,000,000 in fair market value, with a sliding scale between $1,000,001 and $1,500,000. For reference, the rebate reduces by $1,000 for every $10,000 in purchase price above $1,000,000. As an example, a $1,250,000 home would receive $25,000 in GST rebate instead of the full $50,000.

The Federal policy is a permanent legislative change intended to remain in place until at least 2030. Note that eligibility is restricted to first-time buyers.

Provincial level – 8% Ontario PST rebate: The provincial program eliminates the 8% provincial portion of HST, to a maximum of $80,000. For first-time buyers, the provincial rebate is paired with the federal layer on a permanent basis. For move-up buyers and investors, Ontario is funding the federal portion on a cost-sharing basis during the one-year window, which allows non-first-time buyers to also access the full 13% relief from April 1, 2026 through March 31, 2027. During this period, the Provincial level program effectively supersedes the Federal level program. After that date, non-first-time buyers revert to the legacy provincial-only rebate of $24,000.

Qualifying use differs between the two cohorts. First-time buyers must occupy the unit as their primary residence. Move-up buyers and investors may use the unit as a primary residence or as a residential rental.

What is the Rebate

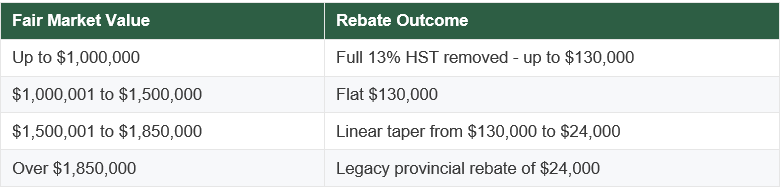

For purchase prices up to $1,000,000, the rebate is based on 13% of HST removed. For purchase prices over $1,000,000, the $130,000 becomes the cap in absolute dollars rather than a percentage of price. This cap extends through $1,500,000 purchase and tapers linearly to the legacy provincial rebate between $1,500,001 to $1,850,000 purchase prices.

The policy effectively functions as a price compression tool around the $1,000,000 mark. Developers pricing above $1,500,000 see progressively less rebate pass-through, which concentrates market activity at and below the $1,000,000 threshold.

How the rebate changes home pricing

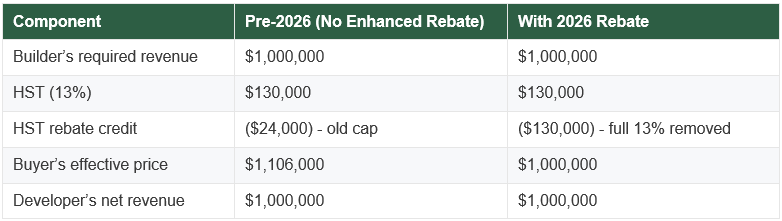

The rebate does not reduce the builder’s required revenue. It shifts the tax carry from the buyer to the government, which allows the developer to lower the advertised price without compressing margins.

Consider a home where the developer’s required revenue is $1,000,000. Under the pre-2026 framework, HST at 13% added $130,000 in tax, offset by the legacy rebate cap of $24,000. The buyer’s effective price was $1,106,000. Under the 2026-2027 program, the same $1,000,000 of builder revenue carries the same $130,000 in HST, but the enhanced rebate now covers the full amount. The buyer’s effective price drops to $1,000,000.

The developer walks away with the same $1,000,000 in either scenario. The buyer saves $106,000, funded entirely by the expanded rebate. This is the mechanism that allows developers to lower prices without cutting margins – and why the rebate can drive new market activities.

Eligibility windows

The program is anchored to three hard dates.

- Agreement of purchase and sale. The APS must be signed between April 1, 2026 and March 31, 2027 for the expanded provincial rebate to apply to non-first-time buyers. Contracts signed outside that window revert the non-FTB cohort to the legacy $24,000 provincial cap.

- Construction start. Construction must begin by December 31, 2028. Projects still in zoning or site-plan approval should be modelling this date against permit, servicing, and excavation timelines.

- Substantial completion. The unit must be substantially complete by December 31, 2031, or December 31, 2029 for owner-built homes. Pre-existing rental projects under construction before March 31, 2026 must complete by late 2029 to remain eligible under the expansion.

Failure to meet any of these deadlines collapses the buyer’s rebate from $130,000 to the legacy amount. Developers pricing units off the enhanced rebate will need to ensure that the project falls within the eligibility windows.

How developers and builders are responding

Many developers are already incorporating the enhanced rebate in their pricing strategies. Here is what we found:

Net-of-rebate pricing. Several large builders are now advertising post-rebate pricing. The buyer contractually assigns the rebate to the builder as part of the APS and the builder handles the CRA application internally. The rebate is marketed as instant savings at closing or framed as additional down payment. However, should the buyer fail to qualify for the rebate, the burden is passed back to the buyer (i.e. a claw back on price difference). This approach maximizes sales activity, compressing the buyer’s mortgage amount and subsequently improving their financing ratios on paper.

Gross pricing with post-closing application. Some mid-sized builders continue to price at the pre-rebate level and direct buyers to apply to CRA independently after closing. This means the buyer has to come up with up to $130,000 at closing and wait for CRA to provide the rebate.

A lender’s perspective

From a construction lending standpoint, the impact of the enhanced rebate is viewed positively; however, it does not materially affect how one would underwrite a project. When reviewing a project proforma, a prudent lender underwrites against the net value of a building rather than the gross value. For reference, net value in this case refers to the expected proceeds that would be available to repay the loan; this is generally calculated by using the gross price less HST, purchaser deposits used in project (if any) and deferred costs (i.e. sales commission, deferred development charges). This approach helps lenders normalize project structures that may defer certain costs to the end, affecting the eventual amounts available to repay the loan.

Should a developer/builder decide to reduce list price on account of the rebate, the project economics do not change given that the net value would be the same. The actual benefit lies in the potential to speed up product absorption, which has largely been stalled over the past few years. Should a developer/builder decide to not pass the benefit from the enhanced rebates to purchasers (i.e. maintaining list price), the additional rebate would improve project economics by either accelerating loan repayment or providing more working capital for the project.

Putting this into practice

In practice, the lender cannot simply assume that the enhanced rebate will be available for the project. The lender should complete due diligence to understand how the enhanced rebate is being incorporated in the developer/builder’s proforma. The due diligence can include but not limited to:

- Assessing if the project construction start and completion will fall within the eligibility window.

- Reviewing the APS to understand how the enhanced rebate will be processed. The APS should incorporate a “Rebate Indemnity” clause in case the purchaser does not qualify for the enhanced rebate.

- Audit purchaser APS to confirm eligibility and that the APS falls within the eligibility window.

Failing to do so can lead to unplanned shortfall in project proceeds 12 to 24 months down the road.

DISCLAIMER

This article reflects Morrison Financial’s understanding of the GST/HST rebate framework as of April 2026. Certain elements – may still be proposed rather than enacted at the time of publication. Program details, eligibility criteria, and timelines may be subject to change. This content is for informational purposes only and does not constitute legal, tax, or financial advice. Consult your legal counsel and tax advisor for guidance specific to your situation.

SOURCES

Aird & Berlis LLP, “2026 Ontario Budget: Enhanced HST Relief on New Homes” (airdberlis.com/insights/publications/publication/2026-ontario-budget–enhanced-hst-relief-on-new-homes); Ontario Budget 2026, Chapter 1B: Costs (budget.ontario.ca/2026/chapter-1b-costs.html); Canadian Private Lenders Association, “Ontario HST New Home Rebate (Proposed) – What Lenders and Brokers Need to Know as of March 25, 2026” (privatelenderassociation.ca); Helio Urban Development, “HST Rebates for Purpose-Built Rentals Explained” (heliourbandevelopment.com/blog/hst-rebates-for-purpose-built-rentals-explained); Canadian Private Lenders Association, “GST/HST New Housing Rebate in Canada: How to Prove Primary Residence Intent After Lisi v. The King (2025)” (privatelenderassociation.ca).

Mortgage Professional, “What Ontario axing the HST on new home sales could mean for the market” (mpamag.com/ca/mortgage-industry/industry-trends/what-ontario-axing-the-hst-on-new-home-sales-could-mean-for-the-market/570101). See also: Mortgage Professional America, “Ontario budget’s housing tax relief draws cautious applause from mortgage and real estate leaders” (mpamag.com/ca/mortgage-industry/industry-trends/ontario-budgets-housing-tax-relief-draws-cautious-applause-from-mortgage-and-real-estate-leaders/570082).

Federal Bill C-4 (Making Life More Affordable for Canadians Act) provides a permanent 5% GST rebate (up to $50,000) for first-time buyers, full to $1,000,000 with a sliding scale to $1,500,000, intended to remain in place until at least 2030. The Ontario 8% PST rebate is permanent for first-time buyers and, during the April 1, 2026 to March 31, 2027 window, is extended on a cost-sharing basis to all eligible buyers including move-up and investor purchasers.