Ontario’s condominium corporations are confronting a structural funding gap. Aging infrastructure, construction cost escalation that consistently outpaces the Consumer Price Index, and an increasingly prescriptive regulatory environment around reserve fund adequacy have converged to undermine the traditional capital planning model.

For boards and their property managers, the implication is clear: reserve funds alone are insufficient to meet the capital demands of the current cycle. When a $5 million window replacement or a $10 million balcony rehabilitation is required, the gap between what the reserve fund holds and what the project costs must be funded from somewhere.

That leaves two paths: a special assessment levied against unit owners, or a condominium corporation loan that spreads the capital cost over time through common expenses. Each has distinct implications for liquidity, governance, and long-term financial planning.

This article is based on Ontario’s legislative framework. Morrison Financial provides condominium corporation loans across Canada – and applies the relevant provincial framework to each transaction.

1. Economic Considerations

The most common objection to a corporation loan is the total cost of interest. Owners will often compare the nominal cost of a special assessment to the all-in cost of borrowing and conclude that the assessment is cheaper. That comparison, while arithmetically correct in isolation, omits three material considerations: the liquidity impact on individual owners, the effect on ownership continuity, and the distribution of financial exposure across the owner base.

1. Liquidity Impact

- Special Assessment: A $50,000 obligation due within 90 days requires owners to liquidate savings, draw on personal credit facilities, or in some cases dispose of the unit itself. The capital call is indiscriminate – it applies equally regardless of the owner’s capacity to absorb it.

- Condominium Corporation Loan: An equivalent obligation of approximately $350 per month, integrated into common expenses, allows owners to service the capital requirement from regular cash flow. The total cost of borrowing over the amortization period will exceed the principal amount – boards should present this transparently alongside the opportunity cost owners would incur to fund an assessment (e.g., HELOC interest, investment liquidation, or personal loan costs).

2. Ownership Continuity

- Special Assessment: A concentrated capital call disproportionately affects owners on fixed incomes and those with limited equity – demographics that are overrepresented in Ontario’s aging condominium stock.

- Condominium Corporation Loan: The monthly debt service component integrates into common expenses, preserving the affordability profile of ownership across income levels.

3.Financial Exposure

- Special Assessment: The full liability becomes payable immediately, regardless of the individual owner’s financial position at the time of the levy.

- Condominium Corporation Loan: The corporation, as borrower, absorbs the capital requirement. Individual owner exposure is limited to a predictable monthly increment in common expenses for the duration of the loan term.

Intergenerational Cost Allocation

A central consideration in any capital funding decision is cost allocation across time. The principle is straightforward: the cost of a long-lived asset should be borne by the owners who benefit from it over its useful life.

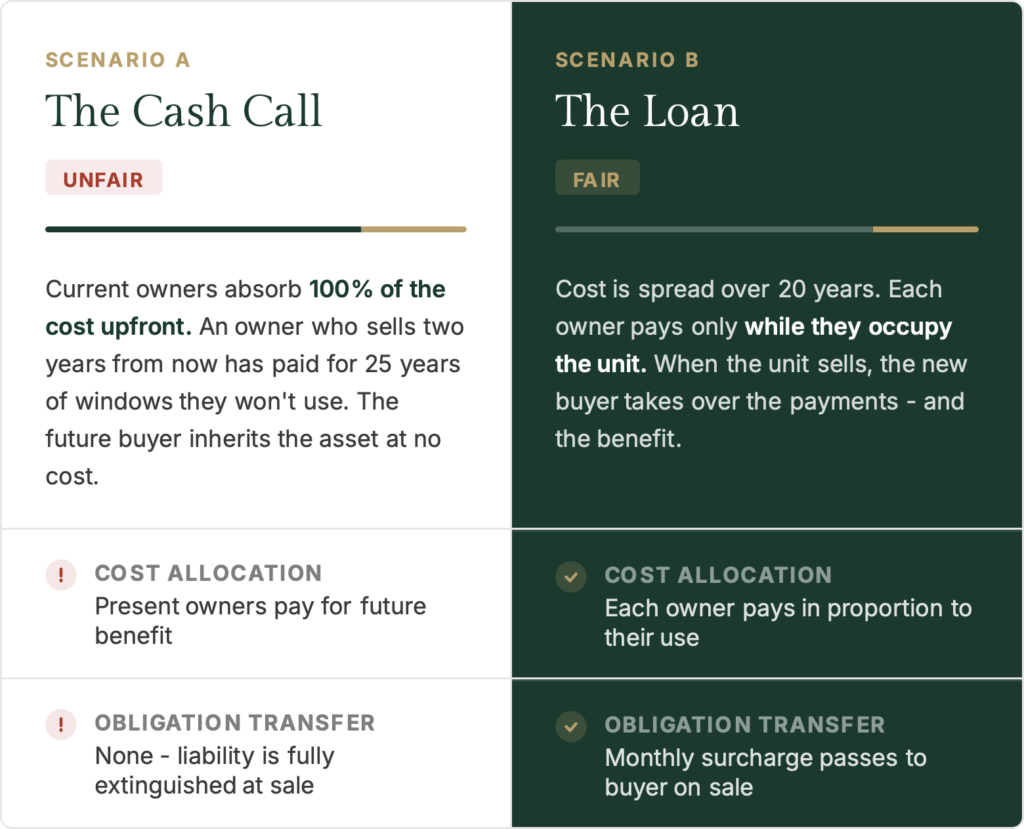

A special assessment front-loads the entire capital cost onto the current owner base. For owners who intend to hold long-term, this may be a reasonable allocation. For owners who sell within a few years of the assessment, the result is less equitable – they bear the full cost of an asset whose useful life extends decades beyond their period of ownership, effectively subsidizing the purchaser who acquires the unit with the repair already funded. Boards should also consider the secondary market impact: a corporation loan appears as a liability on the Status Certificate, and elevated common expenses may affect unit marketability and appraisal values relative to buildings that have already funded their capital requirements through special assessment.

A condominium corporation loan distributes the cost across the asset’s useful life. Each owner contributes only during their period of ownership, and the obligation transfers to the purchaser on sale. This alignment of cost and benefit is the primary structural advantage of the loan model, though it should be evaluated alongside the total cost of borrowing and the potential impact on unit resale values and Status Certificate disclosure.

2. Legal Framework

A condominium corporation loan is extended to the corporation as a legal entity, not to individual unit owners. The borrower is a statutory creature governed by the Condominium Act, 1998 (in Ontario), with borrowing powers that are circumscribed by its Declaration and by-laws. This is a materially different credit structure from conventional commercial lending.

General borrowing authority from the developer era is typically insufficient for a specific capital project. Current practice requires a Specific Borrowing By-Law passed, setting out the purpose of the borrowing, the maximum principal amount, and the term. Boards should confirm the applicable requirements with the corporation’s solicitor, as the interaction between the by-law and the corporation’s Declaration may impose additional conditions.

The following is a general framework. Specific procedural requirements – including quorum, notice periods under Section 47, and any Declaration-specific conditions – should be confirmed with the corporation’s legal counsel:

- Board Approval: The Condominium Board must meet and pass a resolution to create the Borrowing By-Law. The By-Law must specify the purpose of the loan and an upper limit of the amount to be borrowed.

- Notice to Owners: The Board calls a meeting with the owners by issuing a Notice of Meeting, including a copy of the proposed By-Law. An information session or a town hall is typically held to discuss the work required and the financing alternatives available to the corporation, including the terms of a proposed loan.

- Voting: For a By-Law to be confirmed in Ontario, a 50% + 1 vote is required. This represents the majority of owners approving the loan.

- Registration: The By-Law will be in effect once it is registered against the title of the property. the PIN of the corporation.

3. Loan Structure: Distinguishing the Corporation Loan from a Unit Mortgage

A common misunderstanding among owners is that a corporation loan creates a mortgage against individual units. Boards and property managers should be prepared to address this by communicating the following structural features:

- The Condominium Corporation does not own the units, so it cannot mortgage the units.

- The Lender takes an assignment of the Common Expense and Lien rights.

- On a sale, the loan obligation remains with the unit as a component of common expenses. The obligation is not personal to the seller – it transfers to the purchaser, in the same manner as any other common expense obligation.

4. The Opt-Out Structure

In many corporations, the owner base includes both owners who are able and willing to fund their share of the capital cost upfront and owners who require the benefit of term financing. An opt-out clause addresses this by permitting owners to prepay their proportionate share of the loan, while the remaining owners participate in the corporation’s borrowing. This structure broadens the base of support for the by-law by accommodating both constituencies.

Boards should be aware that opt-out structures require the property manager to maintain separate common expense schedules for participating and non-participating units over the life of the loan. This imposes an ongoing administrative burden that affects Status Certificate accuracy and audit complexity. Boards should confirm that their property management firm has the accounting systems and processes to support this structure before adopting it, and should obtain legal advice on the by-law provisions required to implement the opt-out.

5. Owner Communication Framework

Effective owner communication is critical to an informed vote. The following framework may be adapted for the information session or town hall presentation that typically accompanies the by-law process:

- The Building Condition: The engineer or reserve fund study author should present the scope and urgency of the required work, supported by the relevant sections of the reserve fund study or building condition assessment. The objective is to establish the factual basis for the capital expenditure.

- The Financial Requirement: Present the total project cost and translate it to a per-unit obligation under a special assessment scenario, including the timeline for payment (e.g., “The estimated project cost is $3.8 million. For an average unit, this represents a special assessment of approximately $50,000, payable within 90 days of the levy”).

- The Corporation Loan Alternative: Present the terms of the proposed corporation loan and the resulting monthly common expense increase per unit (e.g., “Under the proposed loan, the equivalent monthly cost is approximately $350 per unit, integrated into common expenses over a 20-year term. The total cost of borrowing, including interest, is approximately $x per unit”). Both the monthly amount and total cost should be presented transparently.

- Owner Options: If the by-law includes an opt-out provision, explain how it works and the deadline for exercising the opt-out. Owners should understand that both paths – participation in the loan or prepayment of their share – are available.

A major capital repair project is one of the most significant governance challenges a condominium board will face. A well-structured corporation loan, supported by a properly passed borrowing by-law and clear owner communication, provides a viable alternative to special assessment – one that preserves liquidity, distributes cost equitably, and maintains the financial stability of the corporation. Whether a loan is the appropriate path for a given corporation depends on the specific circumstances, and boards should obtain independent legal and financial advice before proceeding.

Contact us to discuss your situationDISCLOSURE

General Information Only – Not Financial, Legal, or Governance Advice

This article is published by Morrison Financial Services Limited and/or Morrison Financial Mortgage Corporation (collectively, “Morrison Financial”) for general informational purposes only. Nothing in this article constitutes, or should be construed as, financial advice, investment advice, legal advice, governance advice, or a recommendation to pursue any particular course of action, including the decision to borrow. Morrison Financial is a mortgage lender and mortgage brokerage, not a financial advisor, legal advisor, or governance consultant. The information presented reflects general observations based on Morrison Financial’s lending experience and should not be relied upon as a substitute for advice from qualified professionals retained by the condominium corporation.

No Recommendation or Endorsement of Borrowing

This article presents the condominium corporation loan as one capital funding mechanism available to Ontario condominium corporations. It does not constitute a recommendation that any particular corporation should borrow, nor does it endorse borrowing as superior to a special assessment or any other funding alternative. The appropriate capital funding strategy for a given corporation depends on its specific financial position, reserve fund status, building condition, owner demographics, Declaration provisions, and other factors that are beyond the scope of this article. Boards of directors should obtain independent financial and legal advice before making any capital funding decision.

Morrison Financial’s Commercial Interest

Morrison Financial is a commercial lender that originates and administers condominium corporation loans. Morrison Financial has a direct financial interest in the origination of such loans. Readers should consider this interest when evaluating the information presented in this article. The comparisons and frameworks set out herein are intended to illustrate general concepts and should not be interpreted as an objective or independent assessment of the merits of borrowing relative to other alternatives.

Illustrative Figures Only – Not a Loan Offer or Commitment

All dollar figures, interest rates, monthly payment amounts, amortization periods, and other financial parameters referenced in this article are illustrative only and do not represent an offer to lend, a commitment to lend, an indication of available terms, or a quotation. Actual loan terms, including interest rate, amortization, fees, and security requirements, are determined on a transaction-specific basis and are subject to Morrison Financial’s internal underwriting criteria, credit approval process, and due diligence requirements. All lending is at Morrison Financial’s sole discretion.

Total Cost of Borrowing

Any comparison between a special assessment and a condominium corporation loan should account for the total cost of borrowing over the full term of the loan, including all interest charges, fees, and administrative costs. A monthly payment that appears lower than a lump-sum assessment will, over the amortization period, result in a total repayment amount that exceeds the original principal. Boards and owners should compare the total cost of the loan against the actual cost to individual owners of funding a special assessment, including any personal borrowing costs (e.g., HELOC interest, line of credit charges, or investment liquidation costs and tax consequences) that owners may incur to satisfy the assessment.

Legal Framework – Not Legal Advice

This article includes references to the Condominium Act, 1998 (Ontario), including provisions relating to borrowing by-laws, owner notice, and voting requirements. These references are intended as a general overview only and do not constitute legal advice. The procedural requirements for passing a borrowing by-law depend on the specific terms of the corporation’s Declaration, by-laws, and the Act, and may include quorum requirements, notice periods under Section 47 of the Act, and other conditions that are not addressed in this article. A borrowing by-law that does not comply with all applicable statutory and Declaration-specific requirements may be challenged as invalid, which could affect the enforceability of any loan secured by the corporation’s borrowing authority. Boards must retain independent legal counsel to advise on the by-law process.

Opt-Out Structures

Where this article discusses opt-out provisions permitting individual owners to prepay their proportionate share of a corporation loan, such structures introduce ongoing administrative complexity. Maintaining separate common expense schedules for participating and non-participating units over the life of a loan requires robust accounting systems and procedures, and increases the risk of errors in Status Certificates issued under Section 76 of the Act. An inaccurate Status Certificate can give rise to liability for the corporation. Boards considering an opt-out structure should obtain legal advice on the by-law provisions required to implement it and should confirm that their property management firm and auditor have the systems and capacity to administer it accurately for the full term of the loan.

Intergenerational Equity

This article discusses the concept of intergenerational cost allocation as a consideration in the choice between a special assessment and a corporation loan. This discussion is presented as one analytical framework among several. The extent to which a corporation loan achieves equitable cost distribution depends on assumptions about the useful life of the repaired asset, future interest rates, owner turnover, and secondary market conditions, none of which can be predicted with certainty. Morrison Financial does not warrant that a corporation loan will result in a more equitable cost allocation than a special assessment in any particular case.

No Fiduciary or Governance Role

Morrison Financial does not act in a fiduciary capacity with respect to any condominium corporation, its board of directors, or its unit owners. Nothing in this article should be interpreted as defining, advising on, or purporting to discharge any fiduciary duty owed by a board of directors to the corporation or its owners. Directors owe fiduciary obligations under the Act and at common law, and should seek independent legal advice regarding the scope and application of those obligations in the context of any borrowing decision.

Communication Framework

The owner communication framework described in this article is a suggested structure for organizing a presentation to unit owners. It is not a script, a governance recommendation, or a legal compliance tool. Boards are responsible for ensuring that all owner communications comply with the Act, their Declaration, and any applicable by-laws, including notice requirements. The communication framework does not address all matters that may be material to an owner’s voting decision, and boards should ensure that owners receive balanced and complete information – including the total cost of borrowing, the risks of the loan, and the merits of alternative funding approaches – before any vote is held.

Regulatory Status

Morrison Financial Services Limited is licensed as a mortgage brokerage under the Mortgage Brokerages, Lenders and Administrators Act, 2006 (Ontario), Licence No. 10047. Morrison Financial Mortgage Corporation is a mortgage lender. Neither entity is registered as a dealer or advisor under applicable securities legislation, nor is either entity licensed to provide legal advice in any jurisdiction.

No Warranty or Liability

While Morrison Financial has endeavoured to ensure the accuracy of the information in this article as of its date of publication, it makes no representation or warranty, express or implied, as to the accuracy, completeness, or currency of the information. Legislative amendments, regulatory changes, and judicial decisions may affect the applicability of the information after publication. Morrison Financial disclaims all liability for any loss, damage, cost, or expense arising from or in connection with any person’s reliance on the information in this article.

E.O.E.

Effective date: April 6, 2026