Over the past decade, real estate investing has become a highly popularized venture for many Canadians aiming to build long-term wealth. Many simply define real estate investment as the acquisition and ownership of properties, such as ground-oriented homes and condominium apartment units, for rental income and long-term appreciation in value. However, most retail investors are unaware that they can also participate in real estate investment as debt investors. As a prudent investor, it is crucial to understand the difference between equity and debt and their pros and cons to allow one to better adapt their strategy based on risk appetite and market conditions.

Equity Investment:

In its simplest form, an equity investment typically involves purchasing and owning a real estate asset. The return on investment is dependent on the performance of the asset, which can be determined by the sum of any income generated from rental income and appreciation in asset value, less the cost to acquire the asset, and carrying costs (e.g. maintenance, property taxes, mortgage payments). Equity investment is typically considered riskier than debt investment because the investor directly owns the property and is held liable for all ownership obligations and expenses, and the appreciation in value may be speculative.

Debt Investment:

In a debt investment, the investor acts as a lender to provide a loan to purchase the property and/or to improve it. The loan is typically secured by a mortgage, meaning that the underlying asset serves as collateral for the loan repayment. Return on investment is based on pre-agreed interest rates and fees charged for lending the money. Loans that retail investors participate in are typically privately issued (non-bank) to generate an appropriate return on investment.

| Equity Investment | Debt Investment | |

|---|---|---|

|

Participation |

Ownership |

Lender |

|

Typical Timeline |

Medium to long-term |

Short to medium-term |

|

Target Return* |

18% to 25% annualized |

7% to 12% annualized |

|

Cash Flow |

Monthly rental income after expense |

Monthly interest payment |

|

Repayment Priority |

Subordinate to debt |

Priority based on mortgage ranking |

|

Security / Guarantee |

Not applicable |

Mortgage charge on the property |

* For illustrative purposes only. Target return is not guaranteed return and is highly dependent on many factors including types of asset/project, location, security, and market conditions.

Market condition and real estate investment:

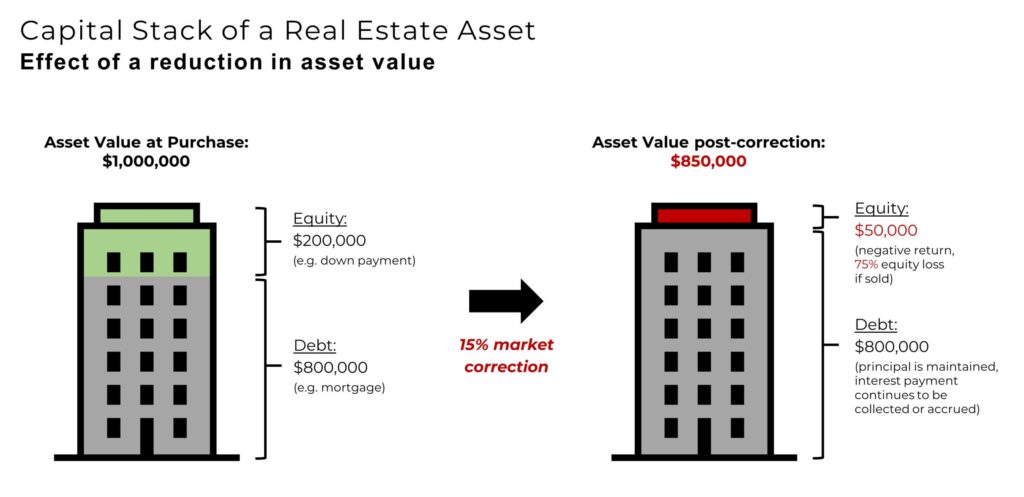

Today’s market condition reinforces the importance of understanding the risks associated with an investment. The recent higher interest rate environment has softened the real estate market and largely impacted equity investments. Real estate investors who are concentrated in equity investments are highly exposed to market corrections as depicted in the diagram below.

The majority of equity investment in real estate is leveraged with debt (mortgage), thereby magnifying its gains and losses. Based on the capital stack illustrated, a 15% market correction would result in a 75% loss on equity investment if the investor is forced to sell the asset. In practice, the 75% loss depicted may be higher after accounting for accumulated maintenance expenses, mortgage payments, real estate commissions, financing penalties, legal costs, etc. On the other hand, debt investment, when properly sourced and managed, can better weather through market corrections and continue to produce returns based on the agreed interest rate and fee with no compromise to the principal investment. Simply put, debt investments prioritize security and predictability over the potential for higher return on investment.

Takeaway:

Investors need to understand and manage risk in accordance with market conditions and individual risk tolerance. Investors who plan to hold an investment long-term and have the capability to withstand a high interest rate environment and market corrections would benefit from higher allocation to equity investment for potentially higher returns. Investors who do not want to be locked into an investment for a long duration and/or require more stability and predictability would find more comfort with a higher allocation to debt investment.